Job losses, pay cuts, force Cambodians into bad debts

VOA Khmer reported on Debts Disaster Cambodia

Sangeetha Amarthalingam

Original Reference: Phnom Penh Post

Publication date 14 May 2020 | 22:04 ICT

The unrelenting negative economic effect of Covid-19 on businesses and banks’ stringent procedures have put Cambodians in a bind over term loans

In the mid-1970s, when the city crashed and burned in a warped socialist uprising led by Communist Party of Kampuchea leader Pol Pot, untold fear gripped the people.

Today, although less menacing, the fear is surreal as Covid-19 does a number on the economy.

It has resulted in thousands of documented job displacements in the garment sector, and wage cuts among white collar workers in Cambodia, although this has yet to be quantified.

The situation is graver because garment workers, as past studies show, stimulate the economy in the informal sector which is made up of street food vendors, hairdressers and transport providers.

A rough estimate shows that each wage earner in the garment sector supports five to six persons in the informal sector via local economic stimulation.

The government estimates that the temporary loss of some 150,000 jobs in the garment sector would indirectly affect some one million people in the informal sector.

David Van, senior associate of Platform Impact, a public-private partnership, said: “The government’s so-called Covid-19 stimulus plan is [also] not leading anywhere as small- and medium-sized enterprises are finding difficulty securing loans.

“If they close shop permanently, then there would be fewer jobs in the future. The picture is very grim.”

As if that was not bad enough, nearly 90,000 Cambodian migrant workers in Thailand who flooded back home amid the crisis will likely raise the unemployment rate in the Kingdom.

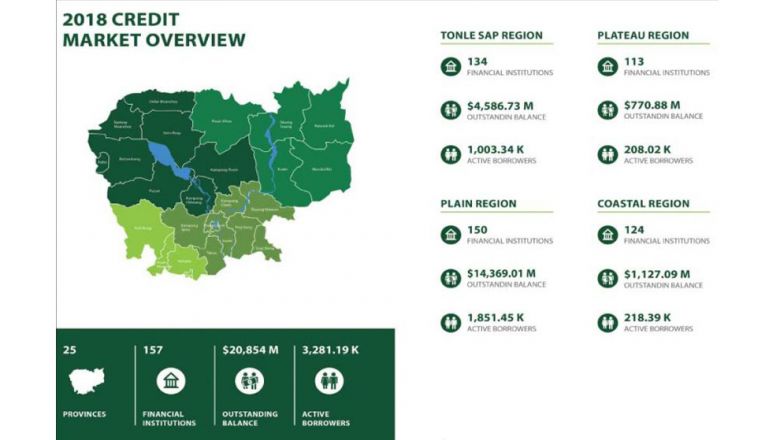

All these could veritably point to an expected growth in indebtedness among Cambodians. Up to 2018, the Credit Bureau of Cambodia recorded $20.9 billion in overall outstanding loan balances, representing 3.3 million active borrowers from 157 financial institutions.

Besides, an updated May report by NGOs Licadho and Sahmakum Teang Tnaut (STT) on the debt crisis faced by the lower strata of the society revealed that more than 2.6 million Cambodian borrowers held more than $10 billion in microfinance debt by the end of 2019.

The report “Driven Out – One village’s experience with microfinance institutions (MFIs) and cross-border migration” said the amount constituted an average loan size of $3,804.

This is supposedly the highest figure in the world, and an increase on an “already troubling” average of $3,370 as of December 31, 2018.

“This debt, the majority of which is collateralised by land titles, continues to pose a significant threat to land tenure security for indebted families and has led to other serious and systematic human rights abuses across the country, including debt-driven migration,” Licadho and STT said.

Based on the report, the situation had already seemed compounding before Covid-19. But the pandemic has sent the Cambodian economy into a tailspin.

The early stage impact was first apparent in the formal workforce starting in February, as minimum wagers lost their jobs after hundreds of factories progressively pulled down the shutters on falling orders and imports of raw material from China.

To date, some 150,000 garment workers have been temporarily suspended and were forced to settle on a third of their monthly income amounting to $70.

Unofficial data states that only 15,000 workers have received state allocation of $40 per person starting this month. The remaining $30 per worker is to be covered by the employers to make up the agreed flat $70 monthly wage for as long as they are temporarily unemployed.

“Of course, suspended workers have been receiving $30 from the companies based on the implementation of the policy [to pay suspended workers $70],” confirmed Garment Manufacturers’ Association in Cambodia (GMAC) secretary-general Ken Loo.

But he refused to divulge the number of affected workers who had received the total $70 salary (which includes the $40).

“It is better you ask the Ministry of Labour. I know the figure but they should say it,” Loo said.

Attempts to contact the ministry to confirm the figure also proved futile.

At last count, 180 factories had closed and another 60 were expected to do the same soon.

It should be noted that the law stipulates that companies can suspend operations for up to two months but they are allowed to extend “if necessary and based on actual situation”.

Whichever way this plays out, the impact on the people has already invoked panic among Cambodians.

The plight of the lower income sector has been judiciously documented in news portals where menial workers in the manufacturing and service industries are reportedly sinking deeper into debt and poverty.

Banks, stern internal rules

The rippling effect of the virus has now spilled into the lower-middle income category, which represents a per capita income of between $1,026 and $4,035 in Cambodia.

In 2016, this growing income level pushed the country up from low income status. By 2030, the Kingdom hopes to achieve an upper middle income economy.

However, the odds are against Cambodians, many who might have been diligently servicing their loans up to now.

Compelling evidence from people interviewed showed that banks were allegedly less than merciful with customers who sought to restructure loans or discuss debt moratoriums.

The hesitance in looking into people’s debts falls out of line with the National Bank of Cambodia’s (NBC) March 27 directive to banks and financial institutions to maintain financial stability, support economic activity, and ease debtors’ burden.

In contrast, neighbouring countries such as Singapore, Thailand and Malaysia have adopted Covid-19 national budgets that define the need for debt refinancing and moratoriums.

On top of that, the stimulus package of these governments involves one-off cash aid to people as well as near-zero interest rate loans.

Suffice to say, Cambodian bankers are treading carefully on the transition based on the complaints of borrowers.

Commenting on this, economist Chheng Kimlong said: “I have seen a few unofficial reports and statistics on this. Some private banks and financial institutions may have their policies and internal rules that are hard to change immediately.

“The government should consider giving enough time to banks and financial institutions as well as some support since they are experiencing revenue losses too.”

“We were crushed”

Requesting anonymity, a couple in Phnom Penh said they raised $20,000 from the lease of their agricultural land measuring 10m by 20m in the city to pay off a hire purchase loan taken with a microfinance institution.

Together with some $5,000 in savings, the debt was repaid, but they were not spared the $500 penalty.

“We pleaded with the officer to excuse the penalty to no avail. We were crushed. We are already low on savings and we have two other loans – a mortgage and hire purchase loan to service monthly,” said the homemaker, whose 42-year-old husband works as a taxi driver.

The $500 sum could have been used to settle one month’s mortgage of $420 with her borey (gated housing development) financing provider, basically the developer which also acts as a building society to housebuyers.

“I have another 15 years to go on my 17-year loan tenure. We are also paying around $360 for another car which my husband uses for work,” said the mother of two teenagers.

But the collapse in the tourism sector essentially rendered her husband, the sole breadwinner of the family, jobless which dampened their debt servicing ability.

Human resource department clerk Sothea (not her real name), foresees dark clouds ahead following her husband’s loss of income from his teaching job in a hospitality school this month.

“The first thing we did was to postpone our $400 monthly mortgage with our developer who provides financial arrangement. We have the option to postpone next month too but I am not sure for how long more.

“Although we postponed the mortgage, we still have to pay about $100 in interest every month,” said the 27-year-old who has a one-year-old son.

She fears that with the current economic condition, her husband, who used to earn about $700 a month, would not be able to secure another job in the short term.

Retail manager Try Sopheak, 34, has had his salary cut by 40 per cent to $800 after sales in the designer clothes shop he works in dropped since late February.

Like the others, he is saddled with a housing loan from a borey financer who has refused to waive the $500 monthly payments which consist of $160 principle amount and $340 in interest.

To add salt to the wound, he is also fined $24 penalty if he pays the loan five days late or $48 if payment is delayed by a month.

The father of two also has a hire purchase loan, and fears that he might not be able to service his loans in the coming months as his employer has indicated a further pay cut.

“I am at a loss over what to do. If I fail to pay my mortgage for two or three months, the developer will seize my house and auction it,” said Sopheak, who owns an affordable house priced at $45,000.

For most borey developments, interest rates on mortgages are exorbitant. In Sopheak’s case, his loan is fixed with a 12 per cent interest rate.

By the end of his 10-year loan tenure, he would have paid $90,000, which is double the house price.

Covid-19, rising debt

The debt situation in Cambodia has been worrying. In 2018, the NBC in its Financial Stability Review flagged the issue of individual debt accumulation which warranted close monitoring.

It warned that a continued increase in overall credit might result in an excessive build-up of individual debt that could potentially have a destabilising effect on the economy.

Backing this is the World Bank’s report on microfinance and household welfare in January last year which found that over the past five years, the average loan size had grown more than tenfold, as did the share of loans for consumption needs and the portfolio-at-risk.

The World Bank said the trends were due to a combination of the low penetration of financial instruments, deteriorating lending practices, and low financial literacy.

Presently, with loss of jobs and pay cuts due to Covid-19, there is no telling how the situation could pan out.

One thing is possible. People are likely to take on more debts to sustain the difficult period, assuming they overcome the bank and MFI’s stringent criteria to secure new loans.

Failing this, they might be pushed to borrow from the unregulated lending market, exposing them to further risks. But all this is conjecture.

Sopheak does not want to end up there, though.

“If things get really bad, I will sell up in Phnom Penh and move to my father-in-law’s village in Kampot and become a rice farmer. That is my exit plan,” he said with sheer resolution.